After the stimulus package for construction industry has been promulgated by the President of Pakistan, a new era of developments is going to begin across the country as builders and developers are all set to invest billions in new construction projects. This sector is open for huge investments from all quarters as FBR will not ask for source of funds invested in construction industry under this package.

As this package entails a number of tax amendments and exemptions for a specified time period, it is important to understand how an individual or a company can avail tax benefits by starting off with a construction project under this scheme.

First we need to understand the tax benefits a company or an individual can avail under this package. Then we will discuss the eligibility criteria and how you can avail these tax incentives.

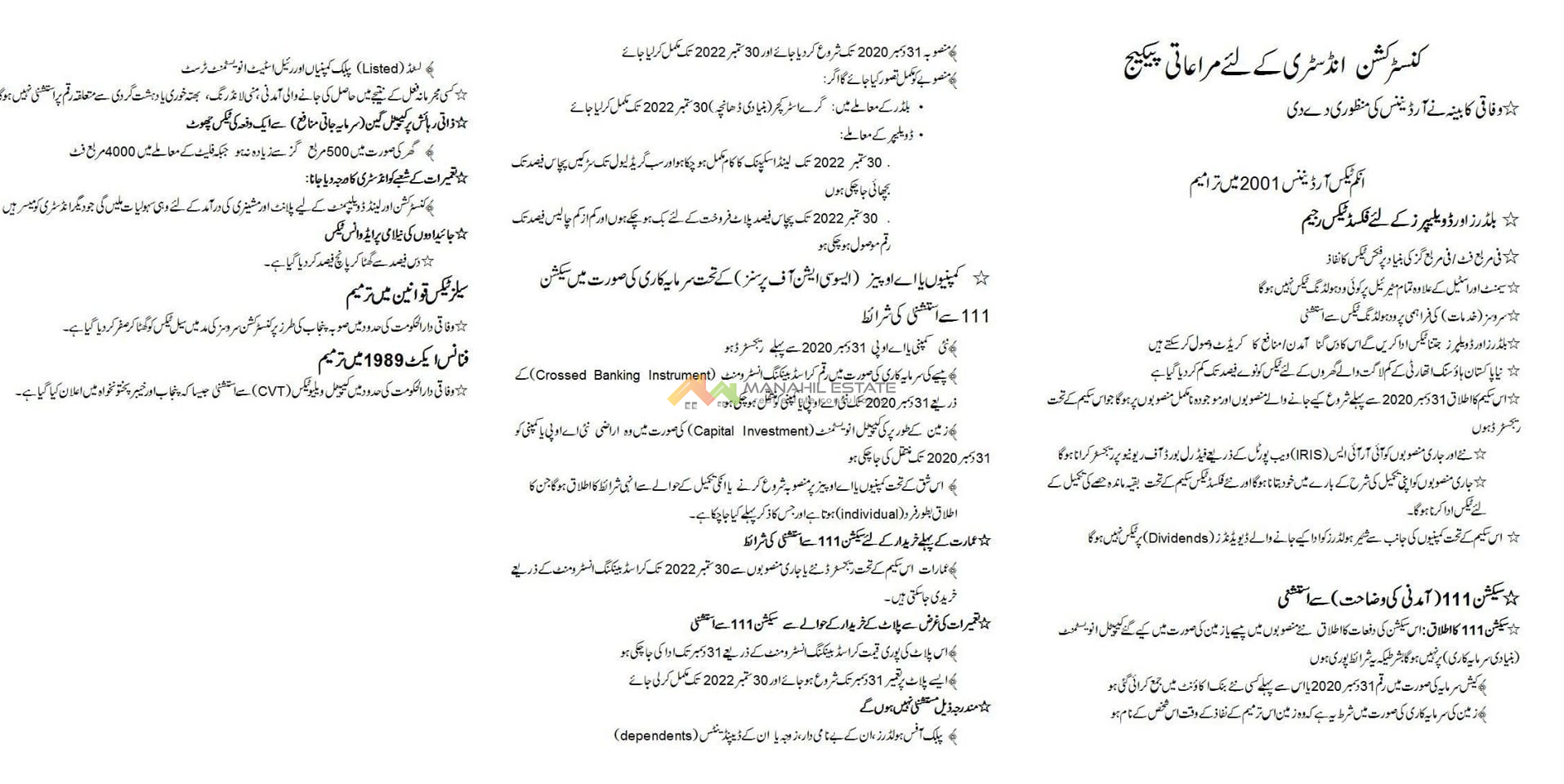

Tax Amendments & Exemptions

Following tax amendments, benefits and exemptions have been announced by the Federal Government under this stimulus package for construction industry:

- Fixed tax regime has been enforced on all development and construction projects. Tax will be charged on per square feet basis in case of building and per square yard basis in case of land development.

- All building materials except Cement and Steels are exempted from Withholding Tax. Similarly all relevant services except those provided by companies are exempted from Withholding Tax.

- Builders & Developers can take credit of profit/income from a project up to 10 times of tax paid. If additional profit is earned, additional tax will be payable.

- Low cost housing projects under Naya Pakistan Housing Development Authority or Ehsaas Program will avail 90% waiver on fixed tax.

- Exemption of tax on dividends paid to shareholders by builders & developers opting for taxation under this scheme.

- Barring a few exceptions (explained under eligibility criteria), capital investment by individuals or companies under this scheme will be exempted from Section 111 of the income tax ordinance, i.e. FBR will not inquire about source of funds.

- One time exemption from Capital Gains Tax in case of sale of personal accommodation provided that house size doesn’t exceed 500 square yards and flat size doesn’t exceed 4000 square feet.

- Advance tax reduced to 5% on auction of properties.

- Sales tax on construction services has been reduced to zero.

- Capital Value Tax (CVT) on purchase of properties has been repealed.

Above tax benefits are not meant just for the construction & development companies, but also for individuals who want to buy a plot and build a house or commercial plaza.

Eligibility Criteria

There are certain eligibility criteria and guidelines which can help you understand how you can register your project under this scheme. Even if you are not a tax filer till date, you can get yourself or your company registered with FBR and make your investment before 31st day of December, 2020 as per the guidelines given in this ordinance.

Any new construction & development project or existing incomplete project can be registered under this scheme provided that it is registered on IRIS web portal of FBR by or before 31st day of December, 2020.

In case of existing incomplete project, the builder/developer will self-declare the percentage of completed work and pay fixed tax for the remaining part.

Exemption from Section 111 of Income Tax Ordinance

The most important part of this scheme is the amendment in section 111 of income tax ordinance which allows you to invest your money without explaining source of funds to FBR. All investments made in construction industry till 31st December 2020 will be exempted from Section 111.

Following conditions must be met in order to be eligible for exemption policy:

- Land for development is purchased before 31st of December 2020. In case of land investment, the land must be under the ownership of the builder at the time of promulgation of this ordinance. In case of cash investment, the amount must be deposited in a bank account and land must be purchased against payment made through the bank by or before 31st December 2020.

- The construction/development project must commence after due approvals and NOCs from relevant development authorities by or before 31st day of December 2020 and the project must be completed before 30th day of September 2022.

- Buildings from the existing or new projects registered under this scheme can be purchased through crossed banking instruments before 30th of September 2022 in order to avail exemption from section 111.

Following individuals/companies will not be exempted from section 111 of income tax ordinance (related to unexplained wealth):

- Public Office Holders, their Benamidars (fake title holders), Spouse and Dependents

- Listed public companies & Real Estate Investment Trusts (REITs)

- Any criminal proceeds derived from Money Laundering, Extortion, and Terror Financing.

You can download complete copy of the Tax Amendment Ordinance 2020 below:

Tax Amendment Ordinance 2020 for Construction Industry

You can read the salient points of the incentive package in Urdu below:

We are quite hopeful that a deluge of black money will be invested in real estate projects in the months to follow that will not only boost real estate prices despite the pandemic blow, but also spur construction activities across the country providing jobs to millions.

Since there is huge demand for low cost houses in the country, builders and developers should also consider developing some low cost residential projects under NPHP. Such low cost units have plenty of potential buyers so the projects will be readily sold and developers will also save 90% on fixed tax.