Property tax has now become one of the most important parts of every real estate transaction in Pakistan. A few years ago, most buyers only checked the demand price, token amount, transfer fee and society charges. In 2026, that approach is not enough.

Today, a buyer must check 236K tax, filer status, late-filer status, non-filer cost, FBR value, DC value, stamp duty, CVT, registration charges, society transfer charges and any other local cost before finalizing a deal. Similarly, a seller must understand 236C tax, capital gain tax position, exemption possibility, documentation requirements and the impact of filer, late-filer or non-filer status.

This guide explains the latest FBR 236C and 236K property tax position for 2026 in a practical Pakistani real estate context. It also explains the expected Budget 2026-27 tax relief package, why high transaction cost has damaged real estate liquidity, and how a reduction in buyer and seller taxes can help revive safe, documented and active property trading in Pakistan.

Important note: Current 236C and 236K rates are based on the existing FBR Tax Year 2026 withholding position. The expected Budget 2026-27 relief is still proposed and should not be treated as final law until approved through the Finance Bill and officially notified by FBR.

Quick Summary for Buyers and Sellers

| Transaction side | Tax section | Who pays it? | Why it matters |

|---|---|---|---|

| Purchase of property | 236K | Buyer / purchaser | Directly increases buying cost at transfer stage |

| Sale of property | 236C | Seller / transferor | Reduces seller’s net amount and affects negotiation |

| Overseas Pakistani case | 236C / 236K | Buyer or seller, depending on transaction | NICOP/POC holders may get filer rate if eligible and verified |

| Budget 2026-27 relief | 236C / 236K | Mainly expected for filers | Can reduce transaction cost if approved |

Before making any token payment, buyers should estimate total transfer cost through the Manahil Estate Property Tax Calculator with FBR & DC Values. Buyers should also cross-check the official taxable valuation through the Manahil Estate FBR Property Valuation Rates Lookup Tool.

What Are 236C and 236K Property Taxes?

In Pakistan, 236C and 236K are advance withholding taxes collected at the time of immovable property transfer. These taxes are collected by the registrar, development authority, housing society, transfer office or relevant authority handling the transfer.

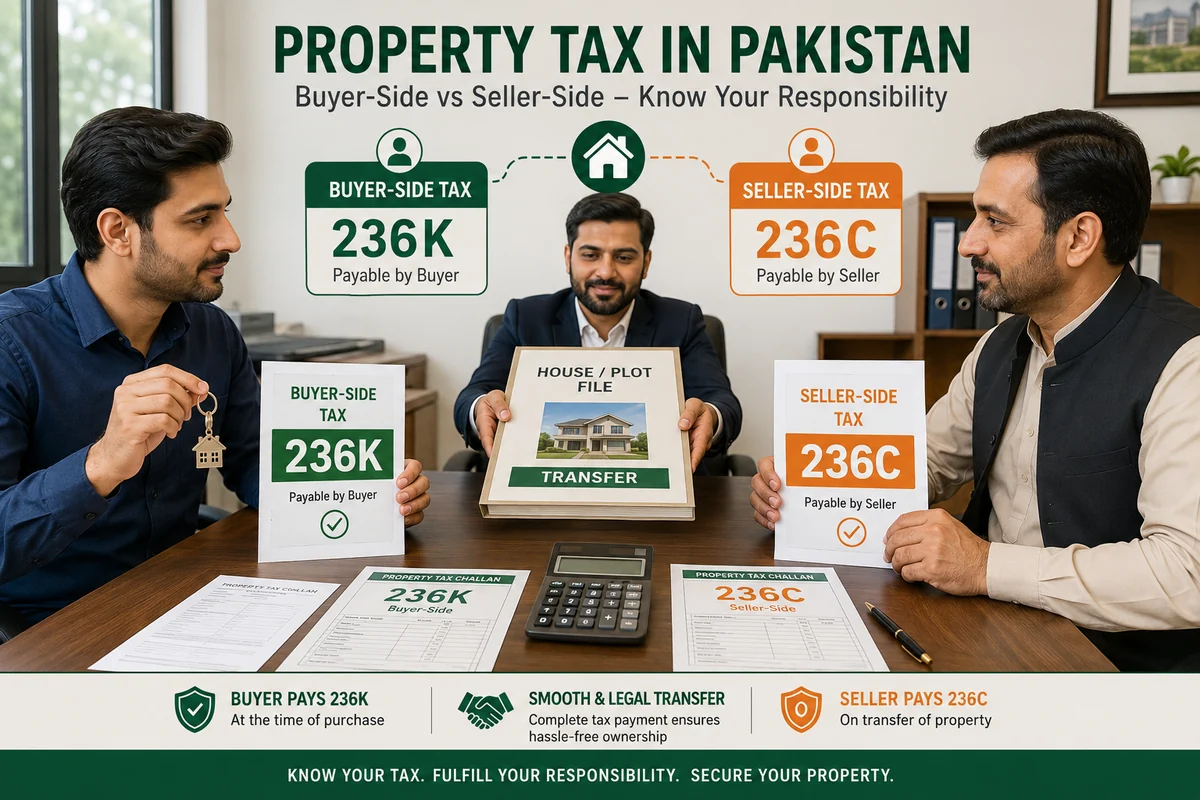

236K: Tax Paid by the Buyer

Section 236K applies to the purchaser of immovable property. In simple words, when you buy a plot, house, apartment, shop, office, commercial property, farmhouse land or any other immovable property, you normally have to pay 236K advance tax at the transfer stage.

This tax is linked with the fair market value or official value used for tax purposes. It is not always calculated only on the private market price agreed between buyer and seller. That is why buyers should never rely on verbal tax estimates. They should check FBR value, DC value and the relevant transfer authority’s charges before paying token money.

236C: Tax Paid by the Seller

Section 236C applies to the seller or transferor of immovable property. When property is transferred from seller to buyer, the seller normally pays 236C advance tax.

For sellers, this is not the only possible tax issue. Capital gain tax, holding period, property type, acquisition date, declared sale value, purchase record, wealth statement record and exemption certificate position may also matter. Therefore, a seller should calculate both immediate transfer cost and annual tax-return impact before quoting a final net price.

Current 236K Rates for Property Buyers in 2026

The current 236K rates are different for filer, late filer and non-filer buyers.

| Fair market value of property | Filer | Late filer | Non-filer |

|---|---|---|---|

| Up to Rs. 50 million | 1.50% | 4.50% | 10.50% |

| Above Rs. 50 million to Rs. 100 million | 2.00% | 5.50% | 14.50% |

| Above Rs. 100 million | 2.50% | 6.50% | 18.50% |

This difference is very large. A filer buying a property valued up to Rs. 50 million pays 1.50%, while a non-filer pays 10.50%. On the same transaction, the non-filer cost can become seven times higher than the filer cost.

Current 236C Rates for Property Sellers in 2026

The current 236C rates for sellers also depend on filer, late-filer and non-filer status.

| Gross consideration / property value | Filer | Late filer | Non-filer |

|---|---|---|---|

| Up to Rs. 50 million | 4.50% | 7.50% | 11.50% |

| Above Rs. 50 million to Rs. 100 million | 5.00% | 8.50% | 11.50% |

| Above Rs. 100 million | 5.50% | 9.50% | 11.50% |

For sellers, the filer rate is also high. A genuine seller of a Rs. 50 million property can face Rs. 2.25 million as 236C withholding tax before considering any other cost. This is one reason many owners delay selling, increase demand to cover tax, or avoid frequent trading.

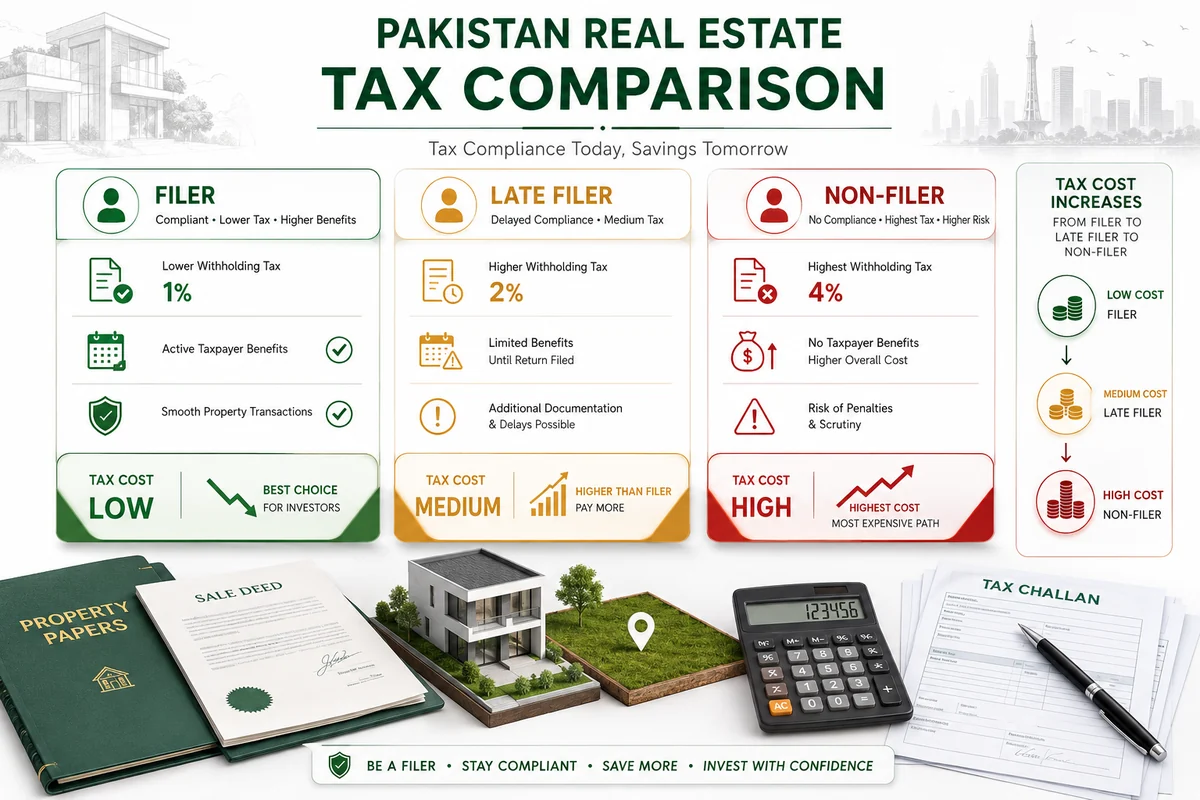

Filer, Late Filer and Non-Filer: Why Status Matters So Much

In 2026, filer status is not a small technical matter. It can completely change the cost of a property transaction.

A filer usually gets the lowest rate. A late filer has filed the return but does not receive the same treatment as an active regular filer. A non-filer or non-ATL person pays the highest rate.

For buyers and sellers, this means one simple thing: check tax status before token payment, not on transfer day.

A buyer should not only ask, “What is the demand price?” The better question is:

“What will be my total transfer cost after 236K, stamp duty, CVT, registration, society charges and other applicable costs?”

Similarly, a seller should not only ask, “What is my sale price?” The seller should ask:

“What will I receive after 236C, possible capital gain tax, transfer expenses and documentation cost?”

Who Actually Bears the Tax Burden in the Market?

Legally, 236K is buyer-side tax and 236C is seller-side tax. But in the real Pakistani property market, the burden often shifts through negotiation.

If the seller’s 236C cost is too high, the seller may increase demand and say, “This is my net price.” If the buyer’s 236K and stamp duty burden is too high, the buyer may reduce the offer. This is how heavy taxes create a gap between buyer expectation and seller demand.

For example, a seller may demand Rs. 5 crore net after tax, while the buyer may calculate that after 236K, stamp duty, registration and society charges, the total cost becomes much higher than budget. Result: the deal does not close.

This is the real damage of high transaction cost. It does not only collect tax. It slows down trading, blocks liquidity, reduces genuine buyer confidence and forces many owners to hold property instead of selling at a realistic price.

Buyer and Seller Scenario Matrix

| Scenario | Buyer position | Seller position | Market impact |

|---|---|---|---|

| Both buyer and seller are filers | Lowest buyer-side 236K | Lowest seller-side 236C | Best environment for a clean deal |

| Buyer filer, seller non-filer | Buyer cost is controlled | Seller faces high 236C | Seller may increase demand to cover tax |

| Buyer non-filer, seller filer | Buyer faces very high 236K | Seller cost is lower | Buyer may back out because entry cost becomes too high |

| Both buyer and seller are non-filers | Very high buyer-side tax | High seller-side tax | Deal becomes difficult unless price is heavily adjusted |

| Overseas NICOP/POC buyer | May get filer rate if eligible and verified | Depends on seller’s tax status | Good opportunity if documents are prepared early |

Practical Example: Rs. 50 Million Property Under Current Rates

Let us assume a property has a taxable value of Rs. 50 million.

Current filer buyer cost under 236K

At 1.50%, the buyer’s 236K tax is:

Rs. 50,000,000 × 1.50% = Rs. 750,000

Current filer seller cost under 236C

At 4.50%, the seller’s 236C tax is:

Rs. 50,000,000 × 4.50% = Rs. 2,250,000

Combined federal withholding pressure

Buyer 236K plus seller 236C becomes:

Rs. 750,000 + Rs. 2,250,000 = Rs. 3,000,000

This means that even when both parties are filers, a Rs. 50 million transaction can carry Rs. 3 million only in these two federal withholding taxes. This does not include stamp duty, CVT, registration charges, society transfer fee, agent service charges, membership fee, development charges or any other cost.

This is why real estate activity slows down when taxes become too heavy. The spread between buying and selling becomes too wide. Investors avoid short-term trading because the entry and exit cost becomes too high.

Expected Budget 2026-27 Relief: Why It Can Be a Major Turning Point

The government is expected to consider a major real estate tax relief package in Budget 2026-27. The reported focus is to reduce transaction cost on property buying and selling, especially for active tax filers.

According to current reports, the main proposals under discussion include:

- 236K buyer tax for filers may be reduced from 1.50% to 0.25%.

- 236C seller tax for filers may be reduced from 4.50% to 1.50%.

- Capital gain tax and other transaction costs may also come under review.

- Measures may be introduced to attract overseas Pakistanis and foreign investment into housing and construction.

- FBR and provincial valuation systems may move toward better alignment to reduce confusion.

Manahil Estate has already covered this development in detail in its report: Budget 2026-27: Real Estate Sector Likely to Get Major Tax Relief in Pakistan.

Important: These are still proposed changes. Buyers and sellers should calculate current taxes first and revise their plan only after the Finance Bill and FBR notification confirm the final rates.

Before and After: How Proposed Relief Can Change a Rs. 50 Million Deal

The real impact of tax reduction becomes clear when we compare current filer rates with the proposed filer rates on a Rs. 50 million property transaction.

| Tax | Current filer rate | Current amount | Proposed filer rate | Proposed amount |

|---|---|---|---|---|

| Buyer tax under 236K | 1.50% | Rs. 750,000 | 0.25% | Rs. 125,000 |

| Seller tax under 236C | 4.50% | Rs. 2,250,000 | 1.50% | Rs. 750,000 |

| Combined burden | 6.00% | Rs. 3,000,000 | 1.75% | Rs. 875,000 |

If approved in this form, the combined buyer-seller burden on a Rs. 50 million filer transaction could reduce from Rs. 3 million to around Rs. 875,000. This is a very big difference.

Such relief can bring investors back into the market because both entry cost and exit cost become more reasonable. A buyer will feel more comfortable entering the market, and a seller will feel more comfortable accepting a realistic offer because the tax deduction will not damage the final net amount as much.

How Lower Taxes Can Revive Pakistan’s Real Estate Sector

Pakistan’s real estate sector does not only need price correction. It needs liquidity. Liquidity means buyers and sellers can transact without excessive friction. When taxes, valuations and transfer charges become too high, trading slows down even in good locations.

1. Lower buyer tax improves entry confidence

If 236K is reduced, buyers can enter the market with a lower upfront burden. This helps genuine home buyers, investors and overseas Pakistanis. A person buying a legally safe possession plot, ready house, apartment or commercial unit can allocate more money toward construction, renovation, rental setup or better location instead of paying a large amount only in transaction tax.

2. Lower seller tax improves exit confidence

Investors do not only calculate purchase cost. They also calculate exit cost. If selling a property is too expensive, investors avoid entering in the first place. Reducing 236C can help sellers accept realistic offers instead of inflating demand only to cover taxes.

3. Lower cost can increase documented transfers

When transaction tax is too high, some market participants try to under-declare value or avoid proper documentation. That is risky for buyers and harmful for the formal economy. A lower but practical tax structure can encourage more documented deals, proper banking channels and clean transfer records.

4. Overseas Pakistanis need clarity and confidence

Overseas Pakistanis can bring strong investment into Pakistan’s housing and construction market. But they need a fair, clear and predictable transfer system. Lower transaction cost, proper NICOP/POC filer-rate processing and transparent valuations can make Pakistan’s real estate more attractive for overseas buyers.

5. Construction and allied industries benefit

Real estate activity is linked with construction, cement, steel, tiles, paint, sanitary, electrical work, labour, transport, furniture, banking and professional services. When property transfers increase and construction resumes, many connected industries also benefit.

This is why property tax relief is not only a benefit for dealers or investors. If implemented properly, it can support wider economic activity.

Overseas Pakistani Property Tax: NICOP and POC Buyers

Overseas Pakistanis are one of the most important investor groups in Pakistan’s real estate market. Many overseas buyers invest in DHA, Bahria Town, CDA sectors, Islamabad societies, Rawalpindi housing schemes, apartments, commercial projects and rental properties. However, tax treatment must be understood properly.

FBR provides a special process for non-resident Overseas Pakistanis holding NICOP or POC. Under this process, eligible overseas Pakistanis can avail filer rates for 236C and 236K even if they are not appearing as regular filers, subject to FBR’s conditions and verification.

Basic eligibility conditions

- The person should hold NICOP or POC.

- The person should be non-resident in Pakistan.

- Non-resident status generally means the person’s stay in Pakistan during the financial year is less than 183 days.

- The required documents must be uploaded and verified through the relevant FBR process.

Practical process at transfer stage

- The registrar, authority or housing society creates the PSID through the overseas Pakistani option.

- The person’s NICOP or POC details are entered.

- Scanned copy of NICOP or POC is uploaded.

- Residence status and supporting documents are submitted.

- The case is routed to the Commissioner Inland Revenue for verification.

- After approval, the system allows payment at filer rate.

This facility can make a major difference. Without proper verification, an overseas buyer may be treated like a non-filer and face a very heavy tax cost. With correct NICOP/POC processing, the same buyer may be allowed to pay at the filer rate.

For overseas clients, the safest route is to prepare documents before token payment, not when the transfer date is already near.

Do Not Confuse Market Price with FBR Value

In Pakistan, one property can have several values:

- Market value

- FBR value

- DC value

- Society transfer value

- Declared sale value

- Bank valuation, where financing is involved

The tax calculation may depend on the relevant official value notified for that area and property category. This is especially important in Islamabad, Rawalpindi, Lahore, Karachi, Peshawar, Multan, Faisalabad and other major cities where official valuation tables are updated from time to time.

For example, a plot in one sector may have a different FBR valuation from another plot in the same society because of possession status, category, road size, location, commercial/residential use, or notified area classification.

For official valuation awareness, Manahil Estate has a dedicated FBR Property Valuation Rates Lookup Tool. You can also read our analysis of FBR revised Islamabad property valuation rates to understand how valuation changes can multiply the tax impact on property transfers.

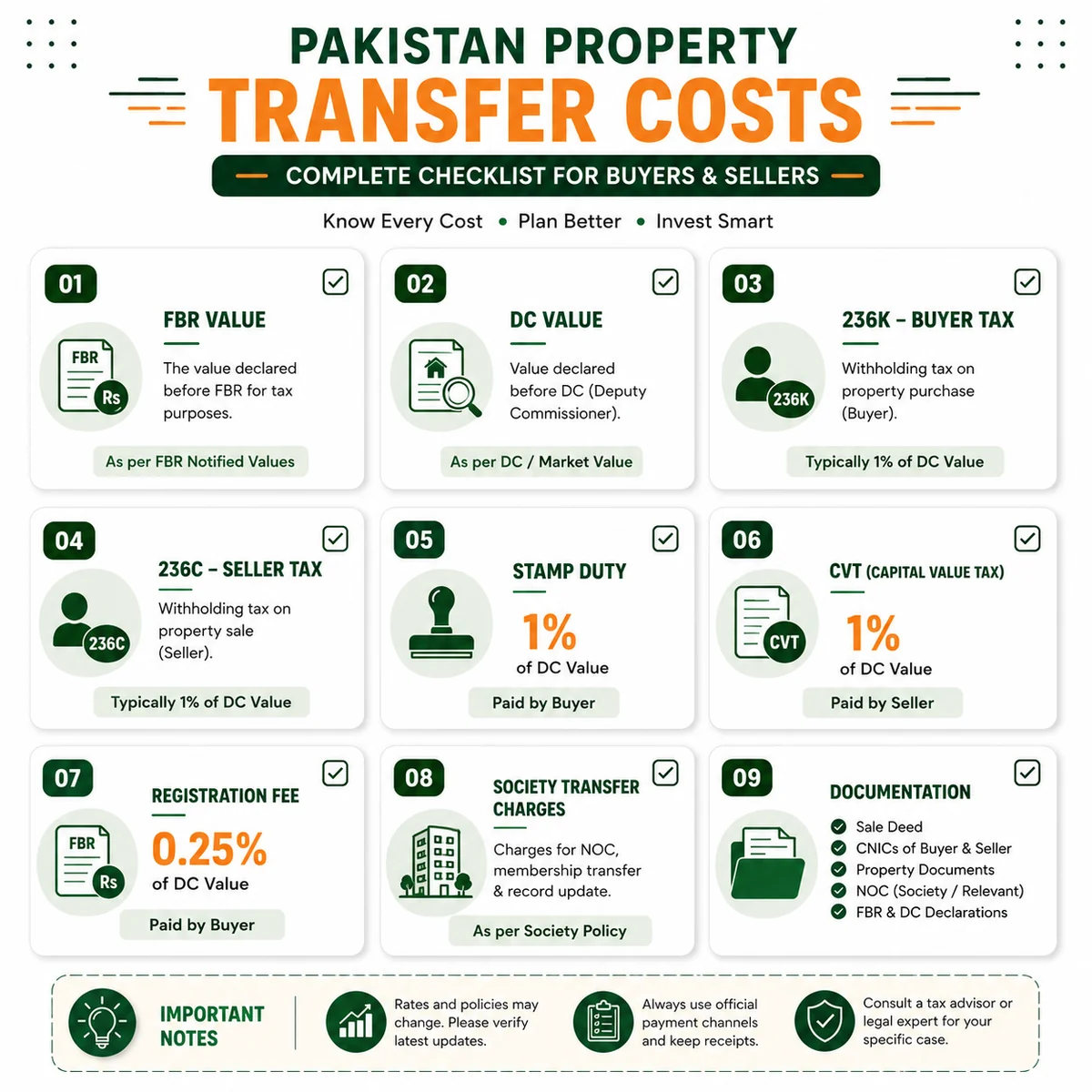

Federal Tax Is Not the Full Transfer Cost

Many buyers make the mistake of calculating only 236K and thinking this is the total cost. That is not correct.

236C and 236K are federal withholding taxes. A complete property transfer may also include:

- Stamp duty

- CVT, where applicable

- Registration fee

- Local government or provincial charges

- Society transfer fee

- Membership fee

- Development charges

- Possession charges

- Utility transfer or clearance charges

- Documentation, verification or mutation charges

- Agent service charges, where agreed

This is why buyers should calculate the full landed cost before making any payment. The Manahil Estate Property Tax Calculator is useful because it helps estimate federal and provincial property taxes together instead of looking at one tax in isolation.

Advance Tax vs Final Tax: What Buyers and Sellers Should Understand

236C and 236K are collected at the time of transfer as advance withholding tax. However, the final tax treatment can depend on the taxpayer’s return filing, property record, gain position, exemption status and latest applicable law.

For buyers, 236K becomes part of the tax record and should be properly reflected in documentation and tax return where applicable. For sellers, 236C should not be confused with complete capital gain tax planning. The seller may still need to review capital gain tax, holding period, cost record and return treatment separately.

In simple words, paying 236C or 236K at transfer stage does not mean every tax question is automatically closed. Proper documentation and return filing still matter.

Can 236C Be Exempted in Some Cases?

In certain cases, an exemption certificate or special tax treatment may be available under law, depending on the taxpayer, transaction type and applicable provisions. This should not be assumed automatically.

A seller who believes an exemption applies should consult a qualified tax adviser and approach the relevant FBR office through the proper legal process. The transfer office or housing society will normally follow the system-generated tax position unless valid exemption approval is available.

For normal buyers and sellers, the safe approach is simple: calculate the tax as applicable first, then separately verify whether any lawful exemption or adjustment is available.

Property Files, Installments, Apartments and Under-Construction Projects

Not every real estate transaction in Pakistan is a simple registry sale of a completed property. Many deals involve society files, allocation letters, installment plans, apartment bookings, commercial units, possession plots and non-possession plots.

This is where buyers must be extra careful.

File transfer and allocation letter cases

In file-based deals, the buyer must confirm whether the file is transferable, whether the allocation is verified, whether installments are clear, and whether any transfer tax or society fee applies at file transfer stage. Some buyers only calculate profit or own amount but ignore transfer and tax cost.

Installment-based projects

In installment projects, the buyer should confirm whether tax is collected on booking, allocation, transfer, possession or final registry. The buyer should also check paid amount, remaining installments, development charges, transfer permission and project approval status.

Apartment and commercial booking transfers

Apartment and commercial projects may involve builder transfer charges, documentation charges, sales tax or other project-specific costs. Buyers should verify whether the project is legally approved and whether transfer is being made through the developer, registrar, authority or private agreement only.

Possession vs non-possession plots

Possession status can affect value, transferability, development charges and buyer risk. Manahil Estate has also covered specific valuation updates such as FBR property valuation updates for Naval Anchorage and Naval Farms, where valuation categories can matter for practical tax calculation.

Buyer-Side Checklist Before Token Payment

Before paying token money, the buyer should complete this checklist:

- Confirm exact property number, sector, block, street and category.

- Check legal status, approval status, possession status and transfer status.

- Verify seller ownership documents.

- Check FBR value and DC value.

- Calculate 236K according to filer, late-filer or non-filer status.

- Add stamp duty, CVT, registration and society transfer charges.

- Confirm whether any development charges, possession charges or utility dues are pending.

- For overseas buyers, prepare NICOP/POC and non-resident verification documents before transfer.

- Keep proof of bank payment, pay order, tax challan and transfer receipt.

- Never rely only on verbal cost estimates.

Buyers can use the Property Tax Calculator with FBR & DC Values before finalizing any token amount.

Seller-Side Checklist Before Transfer

A seller should also prepare properly before accepting token.

- Check current filer or late-filer status.

- Calculate 236C tax on the relevant value slab.

- Review capital gain tax position with a tax adviser.

- Confirm purchase date and sale date for holding-period calculation.

- Check whether any exemption certificate is legally available or required.

- Keep purchase record, allotment letter, transfer letter, sale agreement and payment proof.

- Clear society dues, development charges and utility objections.

- Do not quote a final net price without calculating tax impact.

- Avoid under-declaration because it can create future legal and tax risk.

- Use documented banking channels wherever possible.

Why Investors Are Waiting in 2026

Many investors are currently waiting because of uncertainty. They want clarity on several questions:

- Will 236K be reduced in Budget 2026-27?

- Will 236C be reduced for filers?

- Will non-filers get any relief or only filers?

- Will capital gain tax also be reduced?

- Will FBR valuation tables be revised again?

- Will provincial DC rates and FBR values be aligned?

- Will overseas Pakistanis get smoother processing?

- Will housing finance and mortgage systems become practical?

- Will legal reforms improve property documentation and investor protection?

Until these questions become clear, many investors remain on the sidelines. That is why the next budget and official FBR notifications are very important for Pakistan’s real estate market.

Manahil Estate Advisory: What Buyers Should Do Now

Buyers should not rush blindly before the official package is finalized. However, serious buyers should prepare early.

The better strategy is:

- Shortlist legally safe and possession-based properties.

- Check official valuation and total transfer cost.

- Confirm filer status before token payment.

- Keep funds ready in banking channel.

- Negotiate with tax impact in mind.

- Prefer areas with genuine demand, rental value and resale liquidity.

- Avoid illegal schemes, unclear extensions and unapproved projects.

- For overseas buyers, prepare NICOP/POC and non-resident verification documents in advance.

If taxes are officially reduced, ready buyers will be in a stronger position because they will already understand the market, values and documentation process.

Manahil Estate Advisory: What Sellers Should Do Now

Sellers should also prepare instead of waiting passively.

- Check current filer status.

- Calculate 236C and other possible tax impact.

- Keep ownership documents complete.

- Resolve society dues or transfer objections.

- Confirm realistic market value through recent deals, not only asking prices.

- Decide net receivable amount after tax.

- Avoid unrealistic demand based only on future tax-relief expectations.

- If relief is approved, use the improved market activity to close a clean documented deal.

Common Mistakes in 236C and 236K Property Tax Calculation

Mistake 1: Calculating tax only on market price

Many buyers calculate tax on the negotiated price only, while the official value may be different. Always check the applicable FBR and DC value.

Mistake 2: Ignoring late-filer category

Some people think there are only two categories: filer and non-filer. In practice, late-filer status can create a separate higher tax cost.

Mistake 3: Assuming overseas buyers automatically get filer rate

Overseas Pakistanis with NICOP/POC may get filer rate under conditions, but the process must be followed properly. It is not automatic without verification.

Mistake 4: Ignoring seller-side tax

Buyers often focus only on their own 236K. But if the seller has a heavy 236C burden, the seller may build that cost into the asking price.

Mistake 5: Waiting until transfer day

Tax verification, PSID generation, challan payment and document checking should start before transfer day. Last-minute surprises can delay or damage the deal.

Mistake 6: Ignoring total transfer cost

236K or 236C alone is not the complete cost. Stamp duty, CVT, registration, society charges, documentation charges and pending dues can also affect the final deal.

Mistake 7: Treating proposed relief as final law

Budget expectations can help planning, but a buyer or seller should not finalize a deal only on proposed rates. Always wait for official notification before treating any rate as final.

How Pakistan Can Make Property Transactions Safer and Easier

Pakistan’s real estate market needs a cleaner and more predictable transaction system. Tax reduction is important, but it should be combined with better documentation and digital verification.

The country needs:

- Lower and simpler transaction taxes for documented buyers and sellers.

- Clear online verification of FBR value and DC value.

- Better alignment between FBR valuations and provincial DC rates.

- Digital PSID generation and tracking for all transfer taxes.

- Clear treatment for overseas Pakistanis with NICOP and POC.

- Better rules for file transfers, apartment bookings and installment projects.

- Strong action against illegal schemes and unclear extensions.

- Transparent ownership verification before token payment.

- Consistent documentation standards across societies and authorities.

If Pakistan reduces unnecessary transaction friction and improves verification, more buyers will enter the market with confidence. More sellers will be willing to sell. More investors will trade through proper channels. More overseas Pakistanis will see Pakistani real estate as a safer and more practical investment option.

FAQs

What is 236K property tax in Pakistan?

236K is advance tax collected from the buyer at the time of purchasing immovable property. The rate depends on property value and whether the buyer is a filer, late filer or non-filer.

What is 236C property tax in Pakistan?

236C is advance tax collected from the seller or transferor at the time of property sale or transfer. The rate depends on the value slab and seller’s filer status.

Is a late filer treated the same as a filer?

No. Late filers have separate rates, which are higher than filer rates but usually lower than non-filer rates.

Can an overseas Pakistani with NICOP get filer rate?

Yes. Eligible non-resident Overseas Pakistanis holding NICOP or POC can get filer rate for 236C and 236K under FBR’s verification process.

Are the expected 2026-27 reduced rates final?

No. The proposed reduction in 236K and 236C will become final only after budget approval, Finance Bill changes and official FBR notification.

Should I buy property before or after the budget?

It depends on the property, price, urgency and negotiation. If the deal is strong, legal and below market, waiting only for tax relief may not always be wise. But if transaction cost is the main issue, buyers can calculate both current and expected scenarios before deciding.

What is the safest way to calculate property tax before buying?

Check FBR value, DC value, buyer status, seller status, stamp duty, CVT, registration cost, society transfer fee and any other charges. Use a reliable property tax calculator and confirm final figures with the relevant authority or a qualified tax adviser.

Does 236C replace capital gain tax?

No. 236C is collected at transfer stage, but sellers should separately review capital gain tax, holding period, purchase record and return-filing position.

Does 236K apply to every buyer?

236K generally applies to the purchaser of immovable property, but exact treatment can depend on the transaction type, taxpayer status, exemption position and latest applicable law.

Final Advice

236C and 236K are now central to every property transaction in Pakistan. A good deal is not only about location and price. It is also about legal status, tax cost, documentation, valuation and transfer safety.

For 2026, filers are clearly in a better position than late filers and non-filers. Overseas Pakistanis with NICOP or POC also have an important facility, but they must follow the proper verification process.

If the expected Budget 2026-27 tax relief package is approved, it can improve investor confidence, reduce transaction friction, bring more deals into the documented economy and help revive Pakistan’s real estate sector. Until then, buyers and sellers should calculate taxes carefully, avoid assumptions and complete verification before token payment.

Disclaimer: This guide is for general real estate awareness only. Tax treatment can vary by case, property type, exemption status, return-filing position, latest FBR notification, provincial rules and transfer authority requirements. Buyers and sellers should verify final figures with FBR, the relevant transfer authority or a qualified tax adviser before making payment.

Official and Useful References

- FBR Withholding Tax Rate Card for Tax Year 2026

- FBR FAQs on filer rate under sections 236C and 236K for Overseas Pakistanis

- FBR Valuation of Immovable Properties

- Manahil Estate Property Tax Calculator with FBR & DC Values

- Manahil Estate FBR Property Valuation Rates Lookup Tool

- New Tax Rates Apply for Property Transfers from July 2025

- Budget 2026-27 Real Estate Tax Relief Pakistan

- FBR Revised Islamabad Property Valuation Rates Analysis

- FBR Updates Property Valuation Rates for Naval Anchorage and Naval Farms