For many families in Pakistan, buying a home is not just a dream. It is a long-term financial goal that often feels difficult because of rising property prices, construction costs, and the pressure of arranging a large lump sum amount. This is where government-backed home finance becomes important. The Wazir-e-Azam Apna Ghar Program is designed to make home ownership more accessible for genuine end users through participating financial institutions across Pakistan.

One important point to understand is that this is not a bank-specific product. While different banks may market it with their own branding and brochures, the scheme itself is part of a broader government-backed housing finance framework routed through participating banks and financial institutions. So if you see one bank promoting it more actively, that does not mean the opportunity belongs to that bank alone.

What Is the Wazir-e-Azam Apna Ghar Program?

The Wazir-e-Azam Apna Ghar Program, also known in the market through earlier naming like “Apna Ghar”, “Apni Chat Apna Ghar” & “Mera Ghar Mera Ashiana” under the broader government-backed housing finance framework, is aimed at helping eligible Pakistanis arrange financing for residential property. The main purpose is simple: to support first-time home ownership and make monthly financing more manageable compared to standard market-based borrowing.

This scheme is especially relevant for salaried individuals, young families, and middle-income households who have repayment ability but struggle with the high upfront cost of buying or building a home.

Who Is This Scheme For?

This program is primarily meant for first-time home buyers. In practical terms, it is targeted at genuine end users rather than speculative investors. That is an important difference. In Pakistan’s property market, many people chase files, short-term flips, and paper-based gains. This scheme is more meaningful for people who want a usable house, a flat, or construction support for a home they plan to live in or secure for their family.

For many households, that makes it one of the more practical financing options in the market, especially when compared to risky speculative buying with no clear possession or end use.

What Can the Financing Be Used For?

One of the biggest strengths of this package is that it is not limited to only one type of transaction. Depending on the applicable bank slab and approval, it can generally support different residential needs.

- Purchase of a house

- Purchase of a flat or apartment

- Construction of a house on an already owned plot

- Purchase of a plot along with construction

This makes the scheme useful for both buyers looking for a ready residential unit and families who already own land but need structured support to build.

Islamic Home Finance Option

For buyers who prefer Shariah-compliant financing, this scheme is also relevant because participating Islamic banks offer Islamic home finance versions under the same broader policy framework. In the market, this is often presented through structures such as Diminishing Musharakah, which is one reason the scheme has attracted attention from families looking for an Islamic financing route instead of a conventional one.

This is a valuable point for Pakistani buyers because financing decisions here are not only about affordability. They are also about comfort, trust, and compliance with personal financial preferences.

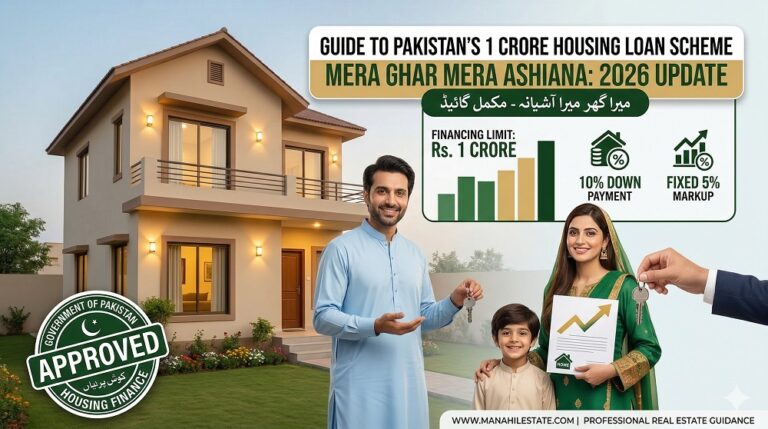

How Much Financing Can Be Available?

In the broader market understanding of this scheme, financing may go up to PKR 10 million depending on the property type, size slab, bank assessment, and the applicable policy tier. Many banks also market this package around houses up to 10 Marla and flats or apartments within the relevant covered area limits.

That said, buyers should not rely only on a brochure or social media creative. The exact financing amount, markup slab, unit size eligibility, and repayment calculation should always be confirmed directly from the latest bank disclosure sheet before applying.

Customer Contribution and Tenor

One of the reasons this program has remained attractive is that it is designed to reduce the pressure of immediate full payment. In general, customers are expected to contribute part of the equity from their own side, while the remaining amount is financed through the bank subject to approval. The repayment period can be spread over a longer tenure, which makes monthly affordability easier for many households.

For end users, this matters more than headline marketing. A buyer should focus on what the monthly installment will look like, what the total own contribution will be, and how the pricing may change after the subsidized period.

Why This Matters in Pakistan’s Real Estate Market

Pakistan’s property market often pushes buyers toward large upfront payments, informal deals, and high uncertainty. A structured housing finance scheme changes that conversation. It gives serious buyers a more disciplined route into ownership, especially in cities and residential areas where genuine housing demand remains strong.

This is particularly useful for people who already have some savings but cannot arrange the full amount for a home purchase or construction all at once. Instead of waiting indefinitely, they can move toward ownership through a formal financing channel, subject to bank approval and legal verification.

In a market where legal clarity and real possession matter, that is an important advantage.

Key Things Buyers Should Check Before Applying

Before applying under this scheme, buyers should verify the latest terms carefully. This is important because bank marketing material can sometimes look simple, while the actual approval process depends on documentation, income assessment, property verification, and the current policy slab.

- Confirm whether you qualify as a first-time homeowner

- Ask the bank for the latest product disclosure sheet

- Check the maximum eligible property size for your category

- Confirm your required own contribution

- Understand the markup structure during the subsidized period and after it

- Make sure the property documents are legally acceptable to the bank

These checks are important because approval is never based on marketing alone. It depends on eligibility, repayment capacity, property legality, and bank credit assessment.

Investor View vs End-User View

From an investor point of view, this scheme is not really about speculative profit. It is far more relevant for genuine residential need. That is why buyers should see it as a home ownership support mechanism rather than a flipping opportunity.

From an end-user point of view, however, it can be a very useful option. If you are planning to buy your first home, purchase a flat, or construct on your own plot, a subsidized and structured financing route can make the decision much more practical.

In simple words, this scheme suits families better than traders.

Final Thoughts

The Wazir-e-Azam Apna Ghar Program is an important housing finance opportunity for first-time home buyers in Pakistan. It should be understood as a policy-backed scheme available through participating financial institutions, not as a single-bank campaign. That distinction matters because many buyers wrongly assume a brochure from one bank means the offer is exclusive to that institution.

For serious home buyers, this program deserves attention. It offers a more practical route toward ownership, especially for people who want a real residential outcome instead of a paper investment. At the same time, applicants should move carefully, verify the latest bank terms, and make sure the property they choose is legally strong and financially manageable.

If used wisely, this scheme can help many Pakistani families take a real step toward secure home ownership.